![]()

CONTRIBUTED BY

Anthony Kappus

anthony.kappus@dlapiper.com

This installment of our series Understanding VC Financing examines liquidation preferences. Along with dividend rights, conversion rights, and anti‑dilution provisions, liquidation preferences are an essential economic term of the preferred stock typically sold in a VC financing.

Liquidation preferences govern how a company allocates and distributes the proceeds from a sale, merger, dissolution, or other liquidation event. The liquidation preference entitles holders of preferred stock to receive distributions of proceeds from an exit transaction before holders of common stock and other series of preferred stock with a lower preference priority and, in certain cases, entitles preferred stock to participate with holders of common stock after payment of the initial preference amount.

The inclusion of caps, multiples and priorities (each discussed below) in structuring liquidation preferences can “reallocate the pie” such that the proceeds of an exit event are distributed differently than the as-converted ownership percentages would imply and/or can indirectly change the effective pre-money valuation being assigned to the company from the perspective of founders and other common stock holders. As such, founders and VC investors should pay careful attention to how liquidation preferences are structured when negotiating the terms of a VC financing.

The three primary components of liquidation preferences are:

(i) what type of transaction triggers the liquidation preference;

(ii) the amount of the initial preference; and

(iii) whether preferred stock participates with common stock, and, if so, whether the participation feature is unlimited (i.e., fully participating preferred) or is subject to a cap or multiple on the return.

Liquidation Events

As the name implies, liquidation preferences apply in the event of an actual liquidation of a company’s assets to shareholders, such as where the company has decided to wind-up operations and distribute assets. However, liquidation preferences are also intended to determine the distribution of proceeds of exit transactions that are not liquidation events such as a merger, stock sale, share exchange or asset sale. Accordingly, liquidation preference provisions usually define these types of change-of-control transactions as “deemed” liquidation events to which the liquidation preference applies.

The Initial Preference

The initial liquidation preference entitles investors to a fixed per share distribution of liquidation proceeds before holders of common stock receive anything. The initial preference is designed to, at minimum, provide downside protection for VC investors and will therefore rarely be less than the amount of investors’ initial per share investment (i.e., if a VC investor buys a share of Series A preferred at $2 per share, the initial liquidation preference will rarely be less than $2 per share). Occasionally the initial preference may also bear a minimum annual rate of return, which is typically a fixed percentage of the original purchase price per share. In my experience this fixed return feature is rare in the current market.

The initial preference is typically also expressed as a multiple (usually 1x, 2x or 3x) of the original price per share paid by the investor. For example, a 2x liquidation preference would entitle an investor that paid $1 per share of preferred stock to a distribution of $2 per share before holders of common stock receive anything. See the chart under “Non-Participating Preferred Stock” for an illustration of the impact of a 1x and 3x initial liquidation preference on the distribution of proceeds of an exit transaction.

Participating v. Non-Participating Preferred

Preferred stock with a participation feature is entitled to continue to receive distributions alongside holders common stock on an as-converted to common stock basis after the initial liquidation preference has been paid. There are any number of ways that participation features can be structured, however, the three most common types of participating preferred stock are:

(a) non-participating preferred stock;

(b) participating preferred stock subject to a cap (e.g. 2x, 3x, etc.); and

(c) fully participating preferred stock.

Non-Participating Preferred Stock

Non-participating preferred stock does not receive distributions along with common stock and is therefore only entitled to the initial liquidation preference discussed above. Accordingly, the only way for holders of non-participating preferred stock to receive a return beyond the initial liquidation preference is to convert into common stock (thereby foregoing the initial liquidation preference).

The following simple example for XYZ, Inc. illustrates the impact of a 1x non-participating preference and a 3x non-participating preference upon the distribution of exit transaction proceeds.

Assumptions for XYZ, Inc.:

- Dollars Invested and Pre-Money Valuation: $5m invested in Series A Preferred Stock at a $5m pre-money valuation ($2.00 per share)

- Outstanding Shares of Common Stock: 2,500,000 (50% of post-closing equity)

- Outstanding Shares of Series A Preferred Stock: 2,500,000 (50% of post-closing equity)

There are two critical valuations: (1) the valuation at which the initial preference is reached (which is also where holders of common stock will start to receive proceeds) and (2) the valuation at which the holders of Series A Preferred would receive greater proceeds if they were to convert to common stock (we call this the inflection point). Between these two valuations (here, between $5m and $10m), holders of Series A Preferred are indifferent as to the exit valuation. This is frequently referred to as the “dead zone” and can lead to misaligned incentives between founders and VC investors and/or among various classes of preferred stock.

There are two critical valuations: (1) the valuation at which the initial preference is reached (which is also where holders of common stock will start to receive proceeds) and (2) the valuation at which the holders of Series A Preferred would receive greater proceeds if they were to convert to common stock (we call this the inflection point). Between these two valuations (here, between $5m and $10m), holders of Series A Preferred are indifferent as to the exit valuation. This is frequently referred to as the “dead zone” and can lead to misaligned incentives between founders and VC investors and/or among various classes of preferred stock.

As the chart illustrates, the larger (3x) initial preference means that holders of Series A Preferred fare much better than holders of common stock at lower exit valuations. Similarly, the “dead zone” is much larger with the 3x preference (valuations between $15m and $30m) than the 1x preference (valuations between $5m and $10m), leading to greater potential for a misalignment of interests between preferred and common holders.

As the chart illustrates, the larger (3x) initial preference means that holders of Series A Preferred fare much better than holders of common stock at lower exit valuations. Similarly, the “dead zone” is much larger with the 3x preference (valuations between $15m and $30m) than the 1x preference (valuations between $5m and $10m), leading to greater potential for a misalignment of interests between preferred and common holders.

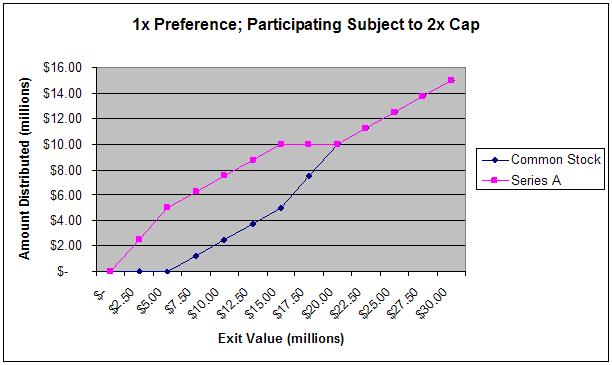

Participating Preferred Subject to a Cap

After receiving the initial liquidation preference distribution, holders of a series of preferred stock with a capped participation feature will share in the liquidation proceeds on a pro rata basis with common stock until the agreed upon return cap is reached. Generally, the cap is a multiple of the original price per share. For example, holders of participating preferred stock with a 1x initial preference and a 3x cap on participation will receive the aggregate of: (i) a distribution equal to their initial 1x liquidation preference and (ii) a pro rata distribution along with common stock until the total amount distributed is equal 3x the initial price per share. It is important to note that the amount of the initial preference is typically included in the cap.

Using the same pre-money valuation and capitalization numbers for XYX, Inc., the following chart illustrates the effect of a participation feature, subject to a 2x cap, on the liquidation waterfall.

Here the three critical valuation points are: (1) the initial liquidation preference amount ($5m), (2) the valuation at which the participation feature caps out ($10m) and (2) the valuation at which conversion to common stock is optimal ($20m).

Here the three critical valuation points are: (1) the initial liquidation preference amount ($5m), (2) the valuation at which the participation feature caps out ($10m) and (2) the valuation at which conversion to common stock is optimal ($20m).

Fully Participating Preferred Stock

After receiving the initial liquidation preference distribution, holders of fully participating preferred will share in the remaining liquidation proceeds on a pro rata basis with holders common stock. The following chart shows XYZ, Inc.’s distribution waterfall with a 1x, fully participating preferred stock:

As the chart illustrates, because there is no cap on the participation feature, there is never an incentive for holders of Series A Preferred to convert to common stock. For this reason, the 1x preference ($5m) is constant and holders of common stock never “catch up” to Series A Preferred holders. Also, because the Series A preferred participates fully alongside common there is no “dead zone.”

As the chart illustrates, because there is no cap on the participation feature, there is never an incentive for holders of Series A Preferred to convert to common stock. For this reason, the 1x preference ($5m) is constant and holders of common stock never “catch up” to Series A Preferred holders. Also, because the Series A preferred participates fully alongside common there is no “dead zone.”

Trends in Liquidation Preferences

We are often asked what “market” liquidation preference terms are. Because liquidation preferences are a fundamental economic term they are highly specific to each company and each deal. That said, we have noticed that while exotic structures with high liquidation preferences and/or generous participation features were very common during the tech boom of the late ‘90s and early ‘00s, in recent years the trend has been towards simpler structures with lower liquidation preferences and low or no participation features. In our view this change is likely driven by changes in founders’ and investors’ expectations of the timing and valuations of exit transactions. During the boom, founders were likely more comfortable with investor-friendly structures because everyone expected high-valuation exits to occur in the near-term. During recent, leaner years as the expected time to exit has stretched out and valuations have come down to earth, founders are less willing to give (and investors to extract) rich liquidation preference terms. The most common liquidation preference structure that we have been seeing this year (though perhaps not rising to a majority of deals) is non-participating preferred stock with a 1x liquidation preference.