![]() CONTRIBUTED BY

CONTRIBUTED BY

Kristi Darnell-Weichelt

kristi.darnell@dlapiper.com

As highlighted in an earlier post, there are a number of factors both buyers and sellers of companies should consider when structuring a purchase and sale transaction. If a buyer and seller have decided to pursue a merger structure (as opposed to, for example, an asset sale, or a purchase of all of the stock of a company directly from the company’s stockholders, each of which has different liability exposures and tax implications), there is still another level of analysis that will need to be performed regarding the actual structure of the merger.

In all merger transactions, one entity legally merges into another entity, resulting in the surviving entity holding all of the assets and liabilities of the merged company. As opposed to an asset sale where assets are formally transferred to another company, the “business” in a merger transaction is acquired by operation of law. Similarly, unlike a direct purchase of stock from a company’s stockholders, a merger transaction typically does not require 100% approval by the target company’s stockholders (the actual approval threshold will be dictated by applicable state law, the target company’s charter documentation, and the terms negotiated into the merger agreement by the buyer and seller).

In this post, we provide a brief overview of the types of merger structures that are commonly used when buying or selling privately-held companies. As always, the descriptions below are not intended to be an exhaustive overview of these structures, and you should consult with your legal and tax advisors before pursuing a merger transaction to be sure you fully understand the consequences of such an approach.

Reverse Triangular Merger

A commonly used merger structure is the “reverse triangular merger.” In a reverse triangular merger, the acquiring company will form a wholly-owned subsidiary company (a “merger sub”). When the merger transaction closes, the merger sub will be merged with and into the target company, with the target company surviving as a wholly-owned subsidiary of the acquiring company. See the graphic below. The stockholders of the target company will receive the consideration offered by the acquiring company (generally cash, stock of the acquiring company, or some combination of each) as payment for “selling” their equity in the target company.

One of the key benefits of a reverse triangular merger structure is the impact (or lack of impact) it has on the licenses and other contracts of the target company. After this type of merger is consummated, a contract between a third party and the target company will remain a contract between the third party and the target company. Most clauses in contracts that bar “assignment” of a contract without the prior written consent of the third party are inapplicable because there has been no transfer of the contractual right from one entity to another entity – in other words, the contract right never left the target company. By contrast, the target company is not the surviving entity in either a direct merger or a forward triangular merger (as discussed below), and as a result, an “assignment” of the contract will generally be deemed to have occurred. As a result, a reverse triangular merger is often preferred when a buyer is seeking to protect the value of contractual rights faster and with greater certainty than is the case, e.g., with the other types of mergers described below, where third parties may withhold consent to the assignment of the contract to the acquiring entity and/or seek a price for providing such consent.

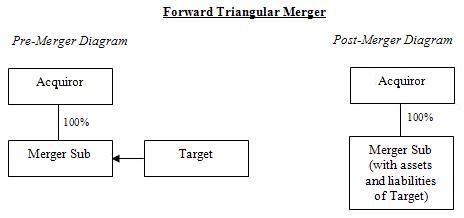

Forward Triangular Merger

A forward triangular merger involves the acquiring company forming a subsidiary company as described above. However, in this type of merger, the target company merges with and into the merger sub, and the merger sub is the surviving entity. See the graphic below. Like the reverse triangular merger, the stockholders of the target company will receive consideration from the acquiring company for the “sale” of their shares in the merger.

Forward triangular mergers, as compared with reverse triangular mergers, are usually less favorable in terms of the non-tax issues (in particular, with respect to the “assignment” issue described above). However, a forward triangular merger has the highest tolerance for non-stock consideration of the available tax deferred merger reorganizations. 50% of the total consideration issued to the target company’s stockholders can be in the form of cash or other non-stock consideration (as opposed to 20% in a reverse triangular merger).

Direct Merger

In a direct merger, the target company merges directly into the acquiring company, with the acquiring company surviving the merger. See the graphic below. The stockholders of the target company will receive the consideration offered by the acquiring company (generally stock of the acquiring company) as payment for “selling” their equity in the target company.

Acquiring companies may view direct mergers as a preferable alternative to a forward or reverse triangular merger for integration and business continuity purposes. However, because the acquiring company is the only surviving entity in a direct merger, the assets and liabilities of the target company are assumed directly by the acquiring company (as opposed to be retained at a subsidiary level, as is the case with a forward or reverse triangular merger). Additionally, in some instances the stockholders of the acquiring company will have approval / appraisal rights in connection with a direct merger (but generally not in the case of a reverse or forward triangular merger), which may add another level of complexity to the transaction.